The top individual and corporate tax rate on investment income goes beyond 50% in most Canadian provinces. This is a shocking reality that many successful professionals and business owners face.

Smart investors have discovered a lesser-known strategy that many financial advisors overlook: building wealth through life insurance. Most people see life insurance as just a death benefit. However, wealthy Canadians recognize that it serves as a powerful, tax-advantaged financial tool.

Life insurance does more than protect your family; it builds wealth, covers final tax liabilities, and protects corporate retained earnings. Permanent life insurance stands out as a "non-correlated asset." Its value stays stable, regardless of stock market conditions.

The strategy's appeal comes from several key benefits under the Income Tax Act (Canada). The cash value in a whole life insurance policy grows tax-advantaged. Your beneficiaries receive the death benefit payout completely tax-free. On top of that, it allows you to protect parts of your investment portfolio from those heavy taxes mentioned earlier.

This piece will show you how to use life insurance as an investment tool and utilize its unique benefits to build wealth. You'll learn everything from leveraging cash value for tax-free capital to protecting corporate assets- strategies that wealthy Canadians have quietly used for decades.

Why Life Insurance Is More Than Just Protection

People often think life insurance just pays out after death. This view overlooks a vital insight: specific life insurance policies work as powerful financial assets that benefit you while you're alive.

Breaking the myth: It’s not just for death benefits

Permanent life insurance combines a death benefit with a savings component that builds cash value over time. Your policy becomes an asset class of its own, much like your RRSP or TFSA, but with different contribution limits and rules. The cash value grows tax-advantaged, and you won't pay taxes on this growth as long as it remains inside the policy. Participating whole life policies also earn dividends that can substantially improve your returns, compounding year after year.

This approach brings great value through its flexibility. The right structure can help you avoid tax liability altogether while giving you access to capital for other investments.

How the wealthy use life insurance differently

Wealthy Canadians see life insurance as a sophisticated wealth-transfer and wealth-creation tool. They don't view premiums as sunk costs, but as asset reallocations.

Affluent individuals and business owners use permanent life insurance to:

- Create tax-sheltered growth: Once RRSPs and TFSAs are maxed out, life insurance provides an alternative environment for wealth to grow without annual taxation.

- Fund deemed disposition: It provides immediate liquidity to cover the CRA's capital gains taxes triggered at death, so heirs don't have to sell valuable assets like the family cottage or business.

- Extract corporate wealth: Business owners use it to move trapped retained earnings out of their corporation tax-free via the Capital Dividend Account (CDA).

Top Strategies to Build Wealth with Life Insurance

Life insurance builds wealth in ways that go far beyond a simple death benefit. Here are eight powerful strategies used by high-net-worth Canadians today:

1. Treat Whole Life Insurance as an Asset Class

Whole life insurance acts as a forced savings vehicle with guaranteed, tax-advantaged growth. Inside the policy, your cash value grows shielded from annual taxation. If you have already maxed out your registered accounts, a permanent life insurance policy offers a powerful alternative to shelter your wealth from Canada’s high investment tax rates.

2. Leverage Cash Value for Tax-Free Capital

Instead of withdrawing money directly from a policy (which can trigger a tax bill in Canada if it exceeds your Adjusted Cost Basis), wealthy individuals use their policy's cash value as collateral for a third-party bank loan. Because you are borrowing against the asset rather than cashing it out, the loan proceeds are entirely tax-free. You can use this capital to invest in real estate or fund a business, effectively putting your money to work in two places at once.

3. Fund Final Tax Liabilities (Deemed Disposition)

In Canada, we don't have an "estate tax," but we do have a deemed disposition tax. When you pass away, the CRA treats all your assets as if you sold them at fair market value, triggering massive capital gains taxes. Life insurance provides your estate with an immediate, tax-free injection of cash to pay this CRA bill, ensuring your heirs don't have to fire-sale the family cottage or business to cover the taxes.

4. Equalize Inheritances

Dividing an estate fairly is rarely simple. For example, you may want to leave a family cottage worth $1,250,000 to one child, and an $850,000 investment portfolio to another. A $400,000 life insurance policy naming the second child as the beneficiary instantly equalizes the inheritance, preserving family harmony without having to liquidate assets.

5. Fuel Corporate Buy-Sell Agreements

For business owners, life insurance is the most cost-effective way to fund a buy-sell agreement. Partners purchase corporate-owned policies on each other. If one partner passes away, the tax-free death benefit flows through the corporation's Capital Dividend Account (CDA), providing the surviving partner the exact tax-free funds needed to buy out the deceased partner's shares.

6. Create a Charitable Giving Plan

You can make a massive charitable impact for a fraction of the cost. By naming a registered Canadian charity as the beneficiary of a policy, or transferring ownership of a policy to them, your estate (or you, while living) receives charitable tax receipts that can drastically offset other tax liabilities.

7. Protect Assets from Creditors

Under Canadian law, life insurance policies generally receive protection from creditor claims, particularly when a specified family member (like a spouse or child) is named as the irrevocable or revocable beneficiary. Your policy's cash value and death benefits can stay safe from seizure, creating a financial safety net during tough economic times.

8. Vary Your Portfolio with Non-Market Assets

Permanent life insurance works as a "non-correlated asset"; its value stays stable despite stock market crashes or real estate downturns. The guaranteed cash value growth delivers dependable returns in any economic climate, balancing an investment portfolio that might otherwise be vulnerable to market swings.

Understanding the Types of Life Insurance

Your wealth-building strategy needs the right foundation.

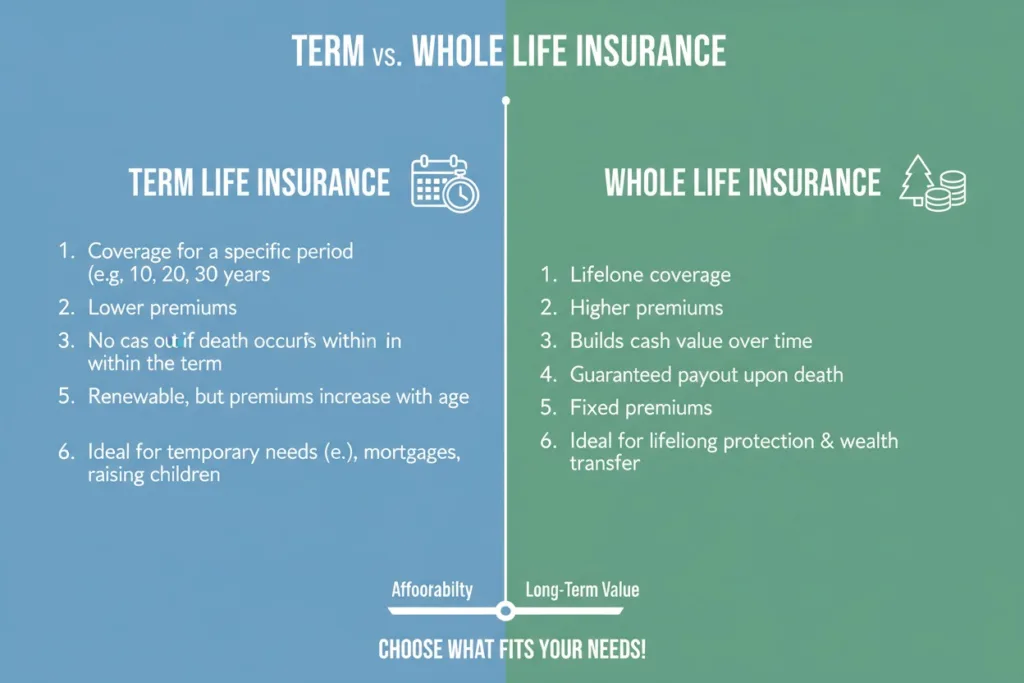

Term vs. Permanent

- Term Life Insurance: Covers you for a set time (e.g., 10 or 20 years). It offers the highest death benefit for the lowest initial cost, but it builds zero cash value. It is pure protection, essentially "renting" your insurance.

- Permanent Life Insurance: Protects you for life. It costs more upfront but features level premiums that never increase, builds accessible cash value, and provides lifelong tax advantages. Whole life and Universal life are the two main categories in Canada.

Why Whole Life is Preferred for Wealth Building

High-net-worth Canadians often choose participating whole life insurance. The policy guarantees growth at fixed rates, avoiding market volatility. Because the cash value is vested, it cannot go down due to market corrections. This creates a rock-solid, liquid foundation for an individual or corporation's broader financial plan.

Advanced Tools for High-Net-Worth Planning

Wealthy business owners and professionals in Canada employ sophisticated financial tools to maximize their corporate and personal wealth.

The Corporate Estate Bond Strategy

Many business owners have surplus cash trapped inside their corporation, facing over 50% passive investment tax rates. Instead of investing in taxable mutual funds, the corporation buys a permanent life insurance policy on the owner. The cash value grows tax-exempt. Upon death, the payout creates a credit to the corporation's Capital Dividend Account (CDA), allowing the proceeds to be paid out to the owner's estate almost entirely tax-free.

Immediate Financing Arrangements (IFA)

An IFA allows high-net-worth individuals or corporations to have their cake and eat it too. You pay the premium into a robust whole life policy, and immediately collateralize it with a bank to borrow back up to 100% of the premium amount. You then use that borrowed money to invest in your business or income-producing real estate. Because you are borrowing to invest, the interest on the loan is generally tax-deductible in Canada, allowing your money to grow inside the policy while simultaneously fueling your other investments.

Choosing the Right Policy and Advisor

These strategies require precision. Setting up a Corporate Estate Bond or an IFA is not a DIY project. You need an advisor who understands holistic financial planning, corporate tax structures, and how to properly design a policy for high early cash value rather than just a high death benefit.

Review your policies regularly as tax laws, your income, and your family dynamics evolve.

Key Takeaways

- Life insurance in Canada is a distinct asset class, offering tax-sheltered growth outside of RRSPs and TFSAs.

- The cash value can be leveraged tax-free to fund real estate or business investments.

- For business owners, it is the ultimate tool to extract trapped corporate wealth via the Capital Dividend Account (CDA).

- It protects your estate by funding the CRA's deemed disposition taxes at pennies on the dollar.

Frequently Asked Questions (FAQs)

Can my corporation deduct life insurance premiums as a business expense?

In most cases, no. The CRA only allows a partial deduction if the policy is explicitly required by a lending institution as collateral for a business loan. However, if you utilize an Immediate Financing Arrangement (IFA) where you borrow against the policy to invest in your business, the interest paid on that bank loan is generally tax-deductible.

Is the cash value growth inside the policy truly tax-free?

Yes, as long as the funds remain inside the policy. Under Canada's Income Tax Act, the growth is "tax-exempt" up to certain limits. If you withdraw the cash directly, it can trigger a taxable event if the withdrawal exceeds the policy's Adjusted Cost Basis (ACB). This is why wealthy Canadians use the policy as collateral for a third-party bank loan to access capital entirely tax-free.

What is the Capital Dividend Account (CDA)?

The CDA is a notional tracking account used by Canadian private corporations. When a corporation receives a life insurance death benefit, the payout (minus the policy's ACB) credits the CDA. This allows the surviving shareholders or the deceased owner's estate to extract those funds from the corporation completely tax-free, bypassing the usual heavy dividend tax rates.

Should I buy Whole Life insurance before maxing out my RRSP and TFSA?

Typically, no. Your RRSP and TFSA are your first line of defense for tax-advantaged growth. Permanent life insurance strategies are best utilized by high-income earners and business owners who have already maximized their registered accounts or have surplus passive income trapped inside a holding company.

How much does it cost to set up an IFA or Corporate Estate Bond?

These are highly customized strategies. The premium depends on your age, health, and the amount of trapped corporate wealth or personal income you want to shelter. Minimum premiums for a properly structured IFA usually start between