Struggling with multiple debt payments each month? If you are an average Canadian feeling the squeeze of inflation and rising interest rates, you are not alone. When credit cards, personal loans, and lines of credit become overwhelming, two of the most popular debt relief solutions in Canada are Debt Consolidation and Consumer Proposals. But how do they differ, and which path should you take?

In this comprehensive guide, we will break down the differences between a debt consolidation loan and a consumer proposal, explaining how each works, their impact on your credit, and how to choose the right strategy to become debt-free.

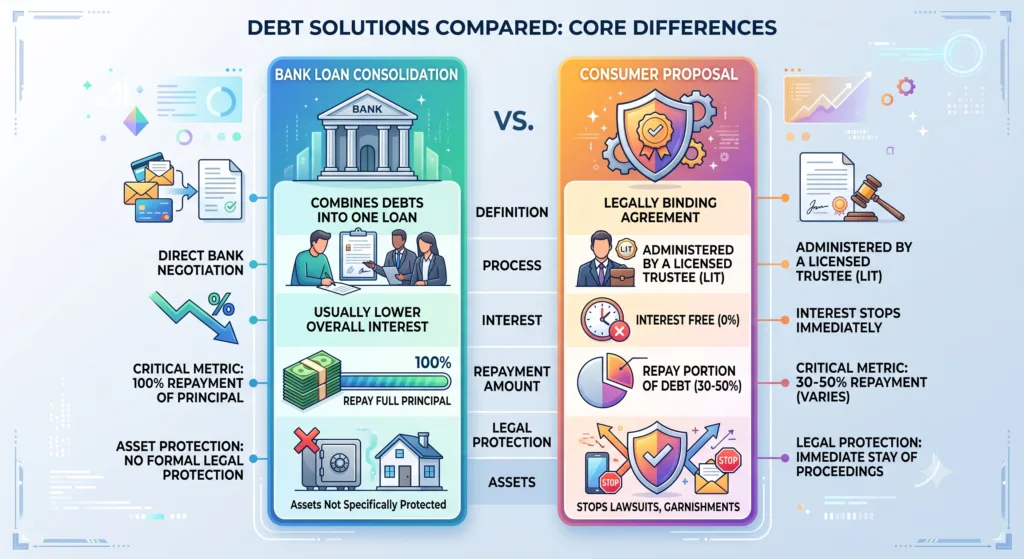

What is a Debt Consolidation Loan?

A debt consolidation loan is a new loan taken out from a bank, credit union, or alternative lender specifically used to pay off multiple existing debts. Instead of juggling five different credit card bills with high interest rates (often 19.99% or more), you consolidate them into a single monthly payment, ideally at a lower interest rate.

How it Works

To get a consolidation loan, you must apply with a lender. The lender will review your credit score, income, and debt-to-income ratio. If approved, the lender pays off your smaller debts, leaving you with one single loan to repay over a fixed term (usually 3 to 5 years).

Key Takeaway: You still owe 100% of the principal debt, plus the new interest rate. The benefit is convenience and potentially lower overall interest costs.

Pros and Cons of Debt Consolidation

- Pros: Simplifies finances into one payment; preserves or even improves your credit score over time; may lower your monthly payment through a reduced interest rate or extended repayment term.

- Cons: Requires a good credit score to qualify; does not reduce the principal amount owed; risks accumulating new debt if you continue using your old credit cards.

What is a Consumer Proposal?

A Consumer Proposal is a legally binding process administered under Canada's Bankruptcy and Insolvency Act. It is not a loan. Instead, it is a formal agreement negotiated between you and your creditors to pay back a percentage of what you owe, forgive the rest, and stop all interest charges.

How it Works

A consumer proposal can only be filed through a Licensed Insolvency Trustee (LIT). The LIT will assess your financial situation and determine what you can reasonably afford to pay. They then submit an offer to your creditors (e.g., offering to pay $15,000 to settle $40,000 of debt). Once a majority of your creditors accept the proposal, it becomes binding on all of them.

Key Takeaway: You pay back a fraction of what you owe (often 30% to 50%), interest is frozen at 0%, and you get legal protection from creditors.

Pros and Cons of a Consumer Proposal

- Pros: Significantly reduces your total debt; stops all interest charges immediately; stops collection calls and wage garnishments; allows you to keep your assets (unlike bankruptcy).

- Cons: Negatively impacts your credit score (an R7 rating stays on your report for 3 years after completion); you must surrender your credit cards; it is a matter of public record.

Key Differences at a Glance

| Feature | Debt Consolidation Loan | Consumer Proposal |

| Principal Repayment | 100% of debt must be repaid. | Usually a fraction (e.g., 30-50%) is repaid. |

| Interest Rates | Lower than credit cards, but still charged. | Frozen immediately at 0%. |

| Qualification | Requires good credit and sufficient income. | For those who are insolvent (cannot pay debts). |

| Credit Impact | Neutral or positive if paid on time. | Negative (R7 rating for 3 years post-completion). |

| Legal Protection | None. Creditors can still pursue you if you default. | Full legal stay of proceedings (stops garnishments). |

Which Option is Right for You?

Choosing between a debt consolidation loan and a consumer proposal depends largely on your current financial health and credit score.

When to Choose Debt Consolidation:

- You have a good to excellent credit score (typically 650+).

- You have sufficient income to repay your total debt, just at a better interest rate.

- You want to protect your credit rating for upcoming major purchases (like a mortgage).

When to Choose a Consumer Proposal:

- You are overwhelmed by debt and cannot make the minimum payments.

- Your credit score is already damaged or you've been declined for a consolidation loan.

- You are facing aggressive collection action, such as wage garnishment or frozen bank accounts.

- You want an alternative to declaring bankruptcy.

The Bottom Line

Both Debt Consolidation and Consumer Proposals are highly effective tools for managing unmanageable debt in Canada. If you have the credit and income to support it, a consolidation loan is an excellent way to simplify your finances while protecting your credit. However, if your debt feels insurmountable and you cannot secure a loan, a Consumer Proposal offers a powerful, government-regulated way to eliminate debt, stop interest, and get a fresh financial start.

Ready to take control of your debt? Reach out to a Licensed Insolvency Trustee or a reputable financial advisor today for a free consultation to review your options.

Frequently Asked Questions (FAQ)

Will I lose my house or car in a Consumer Proposal?

No. Unlike bankruptcy, a consumer proposal allows you to keep all your assets, including your home and car, provided you continue making your regular mortgage and auto loan payments[cite: 1]. Because keeping your assets secure is a top priority, ensuring you have the right home insurance and auto insurance coverage remains essential during this period.

Can I include all types of debt in a Consumer Proposal?

Most unsecured debts can be included, such as credit cards, payday loans, lines of credit, and tax debts owed to the CRA[cite: 1]. Student loans can also be included if you have been out of school for at least seven years[cite: 1]. Secured debts (like mortgages) cannot be included[cite: 1]. If you are looking to secure your family's financial future against these types of outstanding debts, exploring life insurance options is highly recommended.

Do I need a lawyer for a Consumer Proposal?

No. By Canadian law, a consumer proposal can only be filed and administered by a Licensed Insolvency Trustee (LIT)[cite: 1]. They handle all the legal filings and negotiations with your creditors on your behalf. If you have broader questions about protecting your financial health, feel free to contact our team.