Update: The Canadian government officially discontinued the First-Time Home Buyer Incentive (the shared-equity mortgage program) in March 2024. However, powerful tax-advantaged tools like the First Home Savings Account (FHSA) and expanded Home Buyers' Plan (HBP) have taken their place as the primary ways Canadians are saving for their first homes.

First-time home buyers in Canada can now access up to $120,000 tax-free from their RRSPs.

The Home Buyers' Plan lets couples withdraw up to $60,000 each without tax penalties, but this is just one program that helps Canadians buy homes. The First Home Savings Account allows $8,000 in annual tax-deductible contributions with a $40,000 lifetime limit. You can also get a $1,500 rebate through a $10,000 non-refundable First-Time Home Buyer Tax Credit.

Rising housing costs across Canada make these first-time home buyer programs crucial steps toward homeownership. Financial experts suggest keeping monthly housing costs under 39% of your gross income, a target that's harder to reach without government support.

This guide breaks down every first-time home buyer benefit active in Canada for 2026, from federal programs to provincial land transfer tax rebates. We'll show you exactly how to structure your cash flow to make the most of these advantages.

What Are First-Time Home Buyer Grants and Incentives?

First-time homebuyer programs help reduce the financial friction of buying your first home. By combining federal tax breaks with provincial grants, you can significantly reduce your out-of-pocket costs at closing.

How the Government Helps

The government assists home buyers in two main ways today:

- Tax-Advantaged Savings: Accounts that let you grow your down payment faster by shielding it from income tax (like the FHSA and HBP).

- Grants and Rebates: Direct money off your taxes or closing costs, such as the Home Buyers' Tax Credit or provincial Land Transfer Tax rebates.

Why These Programs Matter

House prices remain challenging across Canada. These programs have a simple goal: they help Canadians buy homes faster by accelerating the pace at which you can save a down payment and reducing the immediate cash burden on closing day. By utilizing tax-free growth and deductions, you keep more of your own money working for you.

Step-by-Step Guide to Federal Programs

Canada has four powerful federal programs that help you buy your first home. Here is how you can stack them to maximize your purchasing power:

Step 1: Open a First Home Savings Account (FHSA)

The FHSA is currently the most powerful wealth-building tool for first-time buyers. It gives you the best features of both an RRSP and a TFSA.

You can contribute $8,000 each year up to a lifetime total of $40,000. These contributions are tax-deductible (reducing your taxable income for the year), and you won't pay a single cent of tax when you withdraw the money and its investment growth to buy a qualifying home.

- Your unused contribution room (up to $8,000) moves forward to the next year.

- You can keep your account open for 15 years or until you turn 71.

Step 2: Use the Expanded Home Buyers’ Plan (HBP)

The HBP lets you borrow from your future self by taking up to $60,000 from your RRSP tax-free to fund your home purchase. Couples can access up to $120,000 combined.

You qualify if you:

- Are a first-time home buyer.

- Have a written agreement to buy or build.

- Plan to live in the home as your principal residence within one year.

Key insight: You need to pay back the borrowed amount to your RRSP over 15 years. However, if you make your withdrawal between January 1, 2022, and December 31, 2025, the government has extended the grace period—you now have five years before you have to start making repayments.

Step 3: Claim the Home Buyers’ Tax Credit

Once you buy your home, you can claim the Home Buyers' Tax Credit on your tax return. The credit is valued at $10,000, which translates directly to $1,500 in tax savings.

You qualify if you:

- Buy a qualifying home in Canada.

- Haven't lived in another home you owned in the current or previous four years.

Step 4: Apply for the GST/HST New Housing Rebate

If you are buying a newly built home or heavily renovating one, you can get back some of the GST/HST paid. For homes priced up to $350,000, the federal rebate maxes out at $6,300, and it phases out for homes priced up to $450,000.

Note: Many provinces, like Ontario, offer additional provincial HST rebates on new builds that can save you tens of thousands more.

Planning Ahead: What to Do Before You Apply

Canada has four powerful federal programs that help you buy your first home. Let's look at how you can make the most of each one:

Step 1: Use the Home Buyers’ Plan (HBP)

The HBP lets you borrow from your future self by taking up to $83,601.61 from your RRSP tax-free to fund your home purchase. This higher withdrawal limit works for withdrawals made after April 16, 2024. Couples can access up to $167,203.22 together.

You qualify if you:

- Are a first-time home buyer

- Have a written agreement to buy or build

- Plan to live in the home as your main residence within one year

You need to pay back the borrowed amount to your RRSP over 15 years. The first repayment starts within five years for withdrawals between January 2022 and December 2025.

Step 2: Open a First Home Savings Account (FHSA)

The FHSA gives you the best features of RRSPs and TFSAs. You can put in $11,146.88 each year up to a lifetime total of $55,734.41. These contributions reduce your taxes, and you won't pay any tax when you withdraw the money to buy a home.

Your unused contribution room moves forward to next year. You can keep your account open for 15 years or until you turn 71, whichever comes first.

Step 3: Claim the Home Buyers’ Tax Credit

Once you buy your home, you can claim the Home Buyers' Tax Credit worth $13,933.60 on your tax return. This non-refundable credit gives you about $2,090.04 in tax savings.

You qualify if you:

- Buy a qualifying home in Canada

- Haven't lived in another home you owned in the current or previous four years

Step 4: Apply for the GST/HST New Housing Rebate

You can get back some of the GST/HST paid on a new or renovated home. The maximum federal rebate is $6,300 for homes valued up to $350,000 (the rebate gradually phases out and is reduced to zero for homes valued at $450,000 or more).

Your home must be:

- Located in Canada

- Your primary residence

- Either newly built or substantially renovated

(Note: Depending on your province, you may also qualify for a provincial rebate on top of this federal amount, which can yield significantly more savings!)

Remember to submit your application within two years of the completion date.

Explore Additional Support in Your Province

Canadian provinces complement federal initiatives with their own specialized programs that help reduce home-buying costs—most notably by waiving Land Transfer Taxes (LTT).

Provincial Rebate Examples

| Province | Program | Maximum Benefit |

| British Columbia | First-Time Home Buyers' Program | Full exemption on Land Transfer Tax for homes up to $835,000 |

| Ontario | Land Transfer Tax Refund | Up to $4,000 off the provincial Land Transfer Tax |

| Prince Edward Island | Down Payment Assistance Program | Conditionally interest-free loan up to 5% of purchase price (max $17,500) |

City-Level Incentives

Local municipalities often run their own support programs. For example, Toronto offers its own municipal Land Transfer Tax rebate of up to $4,475 for first-time buyers, which can be stacked directly on top of Ontario's provincial rebate.

Program eligibility and funding change often. The best approach is to check your provincial or municipal housing portals, as many operate on a first-come, first-served basis.

Planning Ahead: What to Do Before You Apply

Getting your financial house in order is critical before you write an offer. These basic steps will boost your approval chances.

1. Check Your Credit Score

Your creditworthiness dictates your mortgage terms. Most conventional mortgages require a minimum credit score of 620 for approval. Your credit score directly impacts the interest rates lenders will offer you—the higher your score, the less you will pay in interest over the life of your loan.

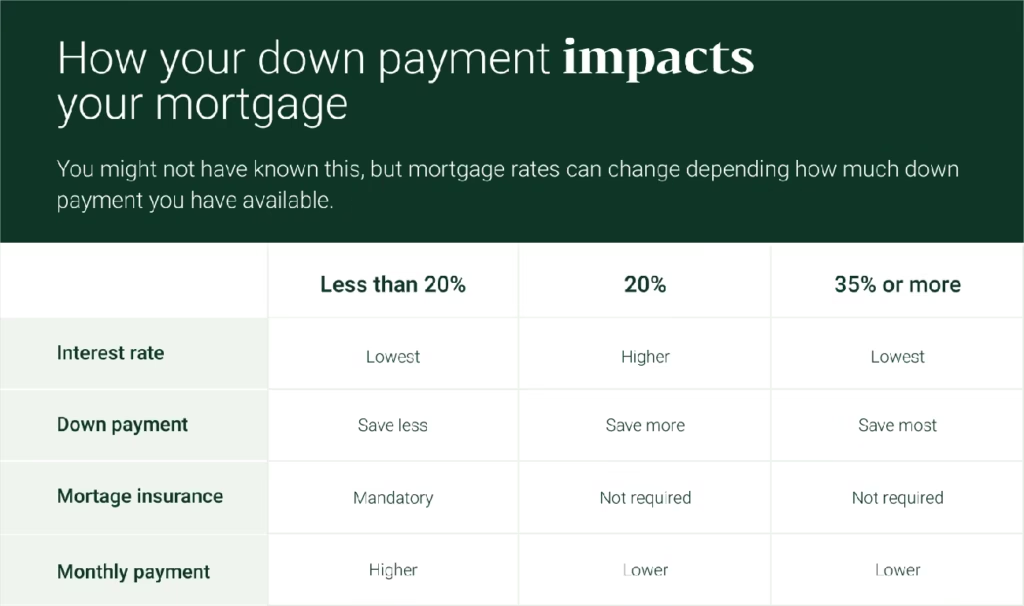

2. Estimate Your Down Payment and Closing Costs

The purchase price determines your minimum legal down payment in Canada:

- 5% for the first $500,000 of the purchase price.

- 10% for the portion between $500,000 and $1,500,000.

- 20% for homes valued at $1,500,000 or higher.

You must also set aside 1.5% to 4% of your home's purchase price for closing costs. These include land transfer taxes (net of any rebates), legal fees, title insurance, and appraisal fees.

3. Get Pre-Approved for a Mortgage

A mortgage pre-approval shows you how much house you can afford and locks in your interest rate for 60 to 120 days. Lenders will verify your income, employment history, and current debt obligations. Staying slightly below your maximum pre-approved amount gives you better monthly cash flow flexibility.

Key Takeaways: First-Time Home Buyer Incentives in 2026

The path to homeownership becomes much easier when you leverage the right tools. Couples can now pull together a massive $200,000 in tax-advantaged down payment funds if both partners maximize their FHSAs ($80,000 combined) and utilize the expanded RRSP Home Buyers' Plan ($120,000 combined).

When you add the $1,500 federal tax credit and provincial land transfer tax exemptions, the savings are substantial.

First-time home buyer programs help you become a homeowner sooner. Take the time to build a holistic financial plan that utilizes these accounts early on. We can help create a custom cash flow strategy that fits your financial situation as you begin this exciting experience of buying your first home.

FAQs

What is the maximum amount a couple can withdraw from their RRSPs for a first home purchase?

As of April 16, 2024, couples can withdraw up to $120,000 combined from their RRSPs through the Home Buyers' Plan for their first home purchase. This allows each individual to access up to $60,000 tax-free.

How does the First Home Savings Account (FHSA) work?

The FHSA allows you to contribute up to $8,000 annually, with a lifetime limit of $40,000. Contributions are tax-deductible, and withdrawals for qualifying home purchases are completely tax-free. Unused contribution room carries forward (up to $8,000 in a given year), and the account can remain open for 15 years or until you turn 71.

What tax benefits are available for first-time home buyers in Canada?

First-time home buyers can claim the Home Buyers' Tax Credit, which is valued at $10,000 and provides exactly $1,500 in non-refundable tax relief. Additionally, the GST/HST New Housing Rebate allows buyers of new builds to recover some of the tax paid. The maximum federal GST rebate is $6,300.

Are there provincial programs available for first-time home buyers?

Yes. British Columbia's First-Time Home Buyers' Program offers a property transfer tax exemption saving buyers up to $8,000. Ontario provides a Land Transfer Tax Refund of up to $4,000, and Prince Edward Island offers loans up to $17,500.